2016 investment strategy is probably one of the simplest since 2008 financial crisis. If you don’t want to take considerable ricks and don’t have time for research but still want to get a decent return – buy USD and put it on deposit or to 1Y treasury bill.

There are not many asset classes in the world which would beat this strategy due to two facts: USD is expected to strengthen against most of the currencies and with the current unpredictability with China GDP slowdown and stock market risky assets returns are very uncertain.

Current state of global economy and financial markets

What happened in 2015?

China

China GDP growth continued to slow down (6.9%E in 2015 vs. 7.3% in 2014)

China started RMB devaluation vs. USD

EMs

Most of EM currencies devaluated against USD

EM economies and financial systems: adjustment vs. defaults as in 1998

Risks of EM USD bonds were overestimated

Divergence in DMs monetary policy: as expected, US FED started rate hikes at Dec 16, 2015 while ECB started QE on March 9, 2015

Europe

ECB QE caused localized stock market boom, which was over mid-April

Greece default had little impact on developed Europe growth, but Eurozone is still almost stagnating

Euro declined to USD: from 1.39 in mid 2014 to ~1.18 at the beginning of 2015 to 1.1 at the beginning of 2016

US

US stock market was immune to EM slow down and potential financial instability in Europe

Number of tech IPOs are declining – indicating only gradual cooling of interest of investors

Commodities haven't bounced back, prices are still declining or under pressure – to a great extent due to China growth slow down and devaluations

2014 was the year when geopolitics came back to the map (Ukraine and Russia). 2015 is the year when the problems have not calmed down and became even more complicated (Syria).

What happened so far in 2016?

China accelerated RMB devaluation

Sell offs on the markets indicated increased uncertainty of investors in Chinese economy

Oil continued to decline due to partly a conflict between Iran and Saudi Arabia and partly due to above mentioned uncertainty about China

Longer term trends

US

US Growth slowed down in the last decade due to lower level of investments. Another way to look at the problem: workers growth and productivity increase growths are slowing down

US has the lowest dependency on goods exports among all the major countries (9.3%) and many US services exports are not easily replaceable

IT and Internet technological revolution has only started. At the same time it transformed to gold rush: too many people are chasing for the same markets, so the best investment area is “tools” and infrastructure for startups rather than startups themselves

US market is the most expensive among major DM markets but the economy has the highest growth potential

Equity markets are now differentiated - correlations between different equity markets are at 10y lows

EMs

EM equity is not growing since 2011

Valuations of many EM countries are below 1 standard deviation of historical averages

India will gradually replace China as a big country still showing similar GDP growth

Due to started FED rate hikes US bonds are from now on are also not a good investment option

Key questions

For 2016

China - is China a systemic risk to the global GDP growth?

How fast will China GDP slow down?

How big will be China RMB devaluation?

Will China valuations decline cause domino effect across the globe as US crisis did in 2008?

Oil – will it bounce back in 2016?

Currencies: will devaluation race happen which didn’t happen in 2008-2009?

Will Fed continue to rise rates? – It will be US economy health indicator. If the FED pauses rate hike for 2016 it would be a very bearish sign

For the longer term: 2016-2018

Will US continue with 2-3% GDP growth?

Which EMs still have growth potential?

If oil doesn’t bounce in 2016, when will it bounce? Current low level of investments and growing demand in case lack of technological breakthroughs make the bounce inevitable. $30/barrel is unsustainable for US shale oil and many traditional producers

Particular asset classes

Will alternative investment classes continue to outperform public equities or their game is over due to big increase in competition?

Will investors’ money stop flowing to VC and will VC valuations collapse?

US commercial Real Estate still shows stable NOI growth (5.7% in Q315) and appreciation (~4%). Will it continue?

Will London residential RE market enter a bear phase?

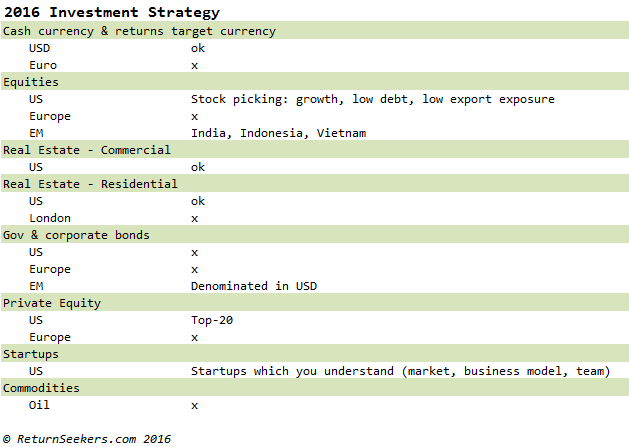

2016 investment strategy

Projections

USD will outperform most of the currencies – currencies of DMs due to growing rates in the US and those of EMs due to continued commodities decline

Most of EMs are out of the game > less growth opportunities > put more money to cash

FED will continue to rise rates

US stocks is the only big attractive pool of risky assets left. FED rate hikes limits market upside, but individual stocks would show attractive returns

No acceleration of global growth + China slow down + devaluations = decline of commodities prices in USD

EMs with good growth: India, Indonesia, Vietnam

Actions

Cash currency and returns target currency in USD

Stock picking among US growth stocks with low export exposure and debt

US RE as an attractive risky asset class

Equities in niche EMs (India, Indonesia, Vietnam)

For those investors who have assess: top-20 US PE&VC funds

EMs USD-denominated bonds: both government and corporate

IT and Internet startups which you understand (=believe in the market, business model, team)

2016 investment strategy is probably one of the simplest since 2008 financial crisis. If you don’t want to take considerable ricks and don’t have time for research but still want to get a decent return – buy USD and put it on deposit or to 1Y treasury bill.

2016 investment strategy is probably one of the simplest since 2008 financial crisis. If you don’t want to take considerable ricks and don’t have time for research but still want to get a decent return – buy USD and put it on deposit or to 1Y treasury bill.